Why the UK will become Europe’s biggest media and entertainment market next year

The UK is set to become the biggest entertainment and media (E&M) market in Europe next year, thanks to online adspend growth and a surge in data consumption.

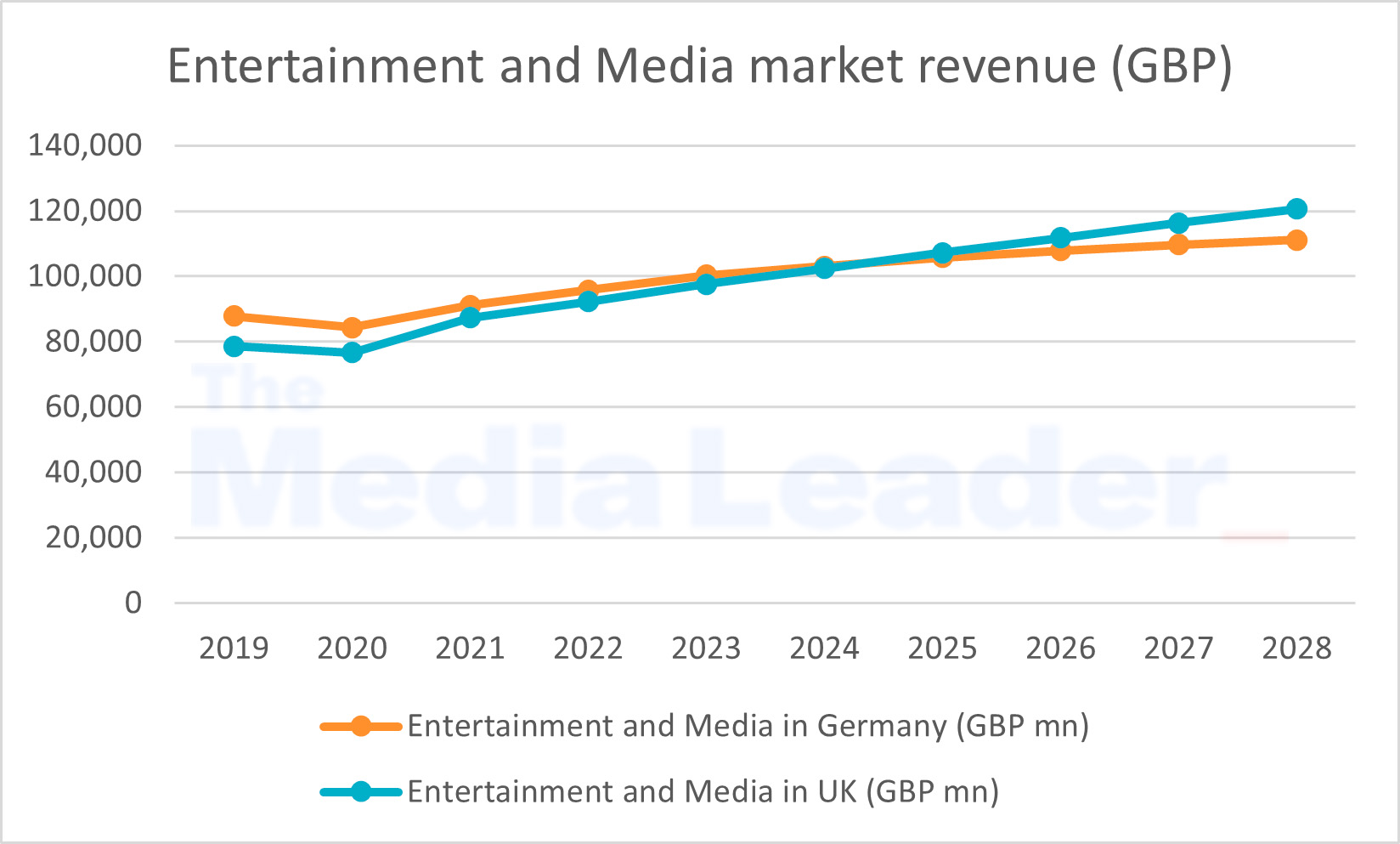

That’s the finding from PwC’s latest Global Entertainment & Media Outlook 2024-2028, which forecasts UK E&M revenue to break the £100bn barrier this year.

E&M revenue will grow to £121bn by 2028, representing a compound annual growth rate (CAGR) of 4%, PwC concluded.

Figures provided by PwC (Click image to enlarge)

Advertising makes up an outsized share of the E&M market in the UK, representing nearly four in 10 (39%) of sector revenue this year, the report said, compared with 29% across Western Europe.

The UK digital advertising market — which PwC estimates to be worth £32bn this year — is forecast to grow to £44bn in 2028. This would mean a CAGR of 8% — among the highest in Europe. Paid search will drive growth within internet advertising, accounting for just over half of total revenue by 2028. PwC attributed this to retail media, which was “rapidly scaling” on paid search.

Mary Shelton Rose, partner and UK technology, media and telecoms leader at PwC, said the UK E&M industry must leverage the power of new and emerging technologies such as generative AI to make the most of future growth opportunities.

“So far, many of the applications of gen AI in the E&M industry have focused on speed and efficiency cost-savings,” Shelton Rose said. “As we look ahead, the industry should further explore how gen AI can lead to greater value creation through experimenting, iterating and scaling new solutions and processes, which can be monetised to drive top-line revenue growth.”

Streaming: One-third funded by ads in five years

By 2028, advertising will account for nearly one-third (30%) of streaming revenue in the UK, up from just under a quarter (24%) this year.

This is due to a “plateauing” of household demand for ad-free subscriptions, the PwC report said, as service providers like Netflix, Amazon Prime Video and Disney+ face increased competition and challenges in getting customers to pay for more services.

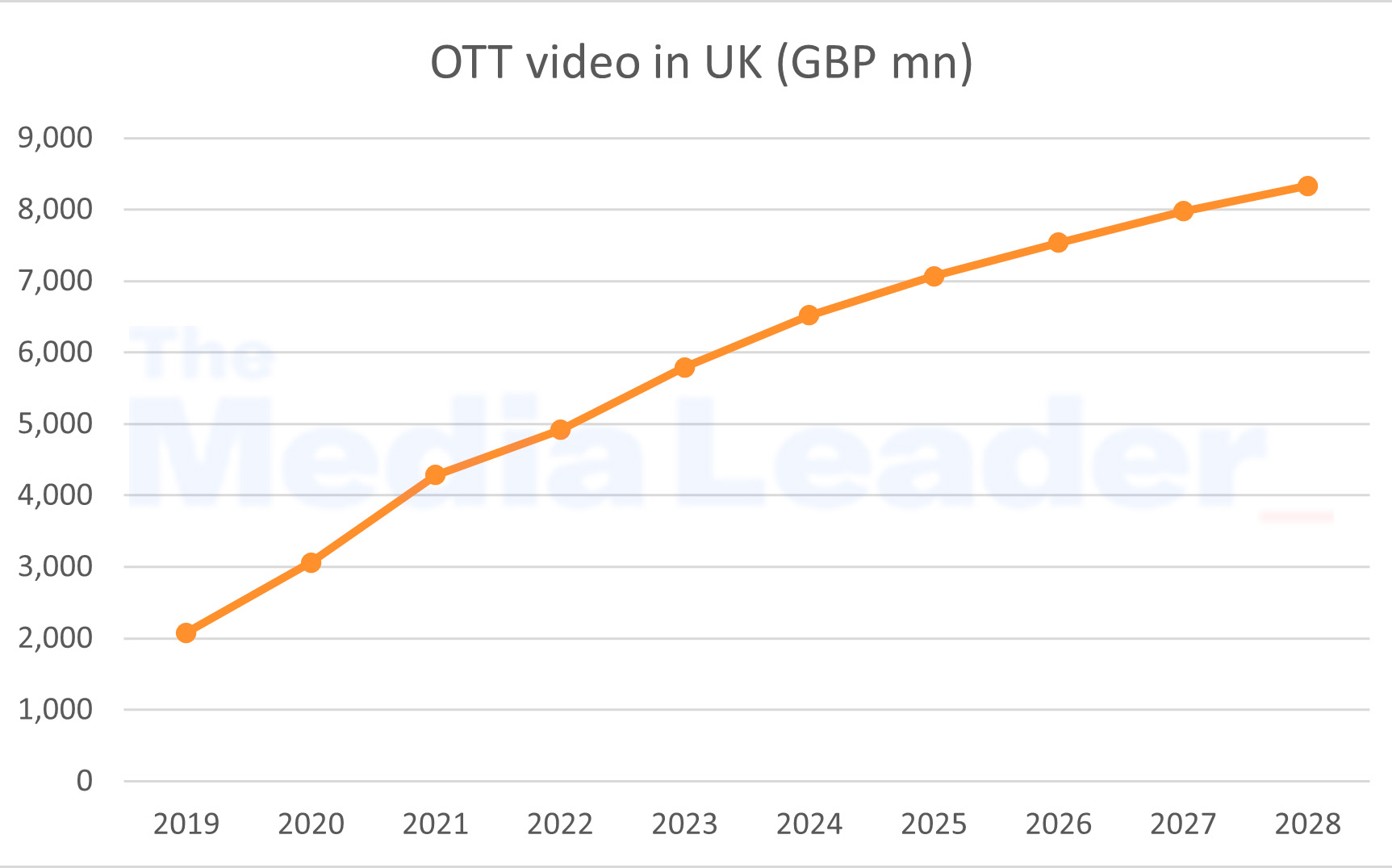

While the volume of “over-the-top” (OTT) video subscriptions per household grew at a CAGR of 20% during 2019-2024, this is expected to slow to a 3% CAGR in 2024-2028. UK subscriptions to OTT video services will rise to £8.3bn in 2028 from £6.5bn in 2024 — representing a 6% CAGR.

Figures provided by PwC (Click image to enlarge)

The UK’s OTT market is the largest in Western Europe and the third-largest globally in terms of revenue, after the US and China.

Ben Bird, E&M sector leader at PwC UK, added: “Prices have risen for several major platforms and, despite the difficult macroeconomic environment, the market has continued to flourish.

“Operators are leveraging their content rights and original productions to boost take-up, leaving consumers needing to subscribe to multiple services or rotate platforms to access the content they desire, such as sports streaming with English Premier League football spread across three streaming platforms.

“The option to have ad-supported plans is also driving growth, in some cases offering the chance to subscribe for slightly less.”

Gaming to grow while cinema will rebound

Total video games and esports revenue is forecast to grow from £7.4bn in 2024 to £8.4bn in 2028 at a CAGR of 3%, the study said.

Social and casual gaming will generate more than half of the UK’s total video games revenue by 2028 due to the availability of games on smartphones, helped by the increasing coverage of 5G mobile internet access in the country.

Meanwhile, total cinema revenue is forecast to continue growing over the next four years at a CAGR of 6%, with cinema admission volumes due to grow at a 5% CAGR. PwC forecasts box office spend to surpass pre-Covid-19 levels in 2027 and by the end of the forecast period be worth £1.3bn.

Live music ticket sales are expected to grow from £1.75bn in 2024 to £1.9bn by 2028 at a CAGR of 1.9%. The sector recovered from the pandemic in 2023, with 2024 experiencing further strong growth, boosted in part by Taylor Swift’s 15 UK performances of the Eras Tour. By 2028, live music will be worth nearly a third (31%) of total music, radio and podcast revenue (£6.1bn).

Marketers should capitalise on an underrated UK export: content

Streaming ad tiers show varying degrees of success in the UK