‘Bullish start to the year’: Media budgets rose in Q1 despite chaotic geopolitics

Total marketing budgets rose at the fastest pace in nearly two years in Q1 2026, despite constant geopolitical unrest and macroeconomic uncertainty. Media budgets have also risen for the first time in four quarters, according to latest IPA Bellwether report.

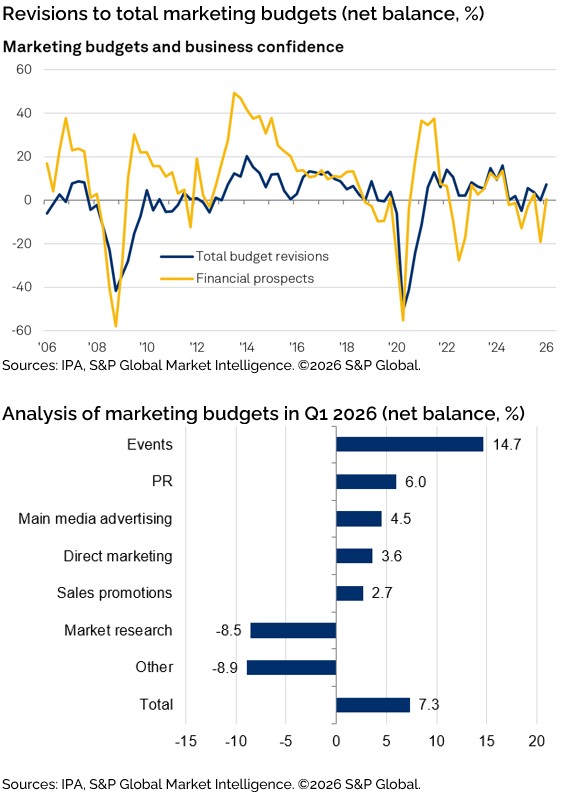

A net balance of +7.3% of businesses surveyed said they had upwardly revised their marketing spend in Q1, a stark increase compared to 0.0% the prior quarter.

The main beneficiaries of growing spend are events (+14.7% net balance) and PR (+6.0% net balance), with the latter potentially benefitting from the growth of AI search causing renewed demand for such services. It also comes as WPP has reportedly begun shopping its PR agency Burson.

Main media budgets meanwhile “encouragingly” rose by a net balance of +4.5% — the strongest upward revision in the category since Q3 2023.

Media budgets notably saw greater investment growth than direct advertising or sales promotions, suggesting brands are more willing to consider longer-term marketing investments despite economic turbulence.

Indeed, the overall increased marketing activity occurred even as UK GDP forecasts have been downgraded, with the US-Israel war with Iran likely to result in substantial global energy shortages and a rise in fertiliser prices, both of which may drive inflation this year and next.

According to the OECD, the UK is facing the biggest hit to growth from the war of the G20 major economies.

Blake Armstrong, managing director of integrated marketing agency Krow Group, points out that the UK hit a 10-year peak in negative consumer confidence in January — “not an anniversary any of us were wanting to celebrate”.

He continues: “This long-standing low consumer confidence is one you would normally associate with a precautionary pulling back of marketing budgets, which historically were the first to go in tough times.”

Nevertheless, S&P Global has upwardly revised its 2026 adspend forecast to +2.5%, compared to a previous forecast of +1.5%, following a stronger-than-expected start to the year for the ad industry.

“Have marketers lost their minds? Have CFOs slipped up? Have client AI agents gone rogue? The answer is no,” Armstrong tells The Media Leader. “For businesses under pressure to deliver growth, the price of inaction is far greater than making a mistake. Companies need marketing now more than ever to beat the market conditions and drive growth, so are therefore spending accordingly.”

‘Moving beyond short-term performance’?

Paul Bainsfair, director general of the IPA, agrees that the results “defy wider geopolitical uncertainty”, adding they “signal a bullish start to the year for UK marketing investment”. He takes special pleasure in main media budgets specifically rising.

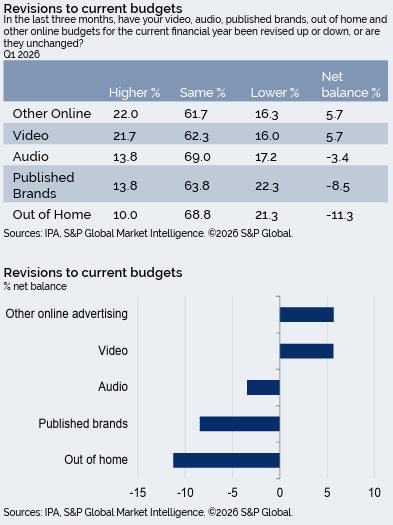

Within main media budgets, growth is being driven by an uptick of businesses investing in video and continued growth, albeit a deceleration, in budgets for other online advertising.

“The evidence is being heeded, even in tougher conditions: cutting back on advertising risks long-term damage,” Bainsfair continues. He praises UK businesses for “holding their nerve” and investing in media to stay front of consumers’ minds and strengthen their brands.

A net balance of 5.7% of firms increased investment in both categories last quarter. This amounts to a substantial upward revision in video budgets compared to Q4, when a net balance of firms (-5.0%) decreased investment in the channel.

In comparison, online advertising growth was slower compared to the +13.2% net balance of firms that increased investment in the channel in the prior quarter.

Other media categories continued to see downward revisions in the net balance of firms investing, however. Audio budgets were revised down for the twelfth consecutive quarter (-3.4%), though this is the highest reading in the past three years.

Publishing brands likewise saw a decline in net revisions to marketing budgets of -8.5%, down from -6.5% in the previous quarter. This is the lowest net balance recorded for the media channel since Q4 2024.

However, the largest drag on main media marketing spend continued to be OOH for the fifth straight quarter (-11.3%).

“It’s encouraging, but the underlying channel dynamics remain consistent with past quarters, including the continued growth in events, PR and digital, alongside ongoing pressure to more traditional, harder-to-measure media such as OOH, audio and print,” remarks Jon Chamber, director of investment at independent agency Generation Media.

“The uplift in main media spend indicates brands are beginning to re-engage with broader reach channels, but investment remains selective and closely tied to provable outcomes.

Jockeying for market position amid tumult

Mallory Simmonds, the recently-appointed CEO of Jungle Creations, agrees that advertisers are generally scaling budgets in media channels only once effectiveness is proven to the brand.

“The demand for measurability, which was accelerated by market contraction, will continue even as that pressure eases,” she adds, arguing that “nowhere is this clearer than in social, which is no longer viewed just as a venue for scaled engagement, but as a core driver of revenue growth.”

Despite the rosy Q1 picture, Bellwether respondents say that the US-Israel war with Iran is likely to exert downward pressure on business senitment. Companies, the report notes, are already seeing tangible spillover effects, namely through higher input costs and disruptions to shipping and supply chains.

Respondents also linked uncertainty caused by the war to delayed decisionmaking and investment, such as for high-level purchasing decisions, hiring, and M&A activity.

With this backdrop, Maryam Baluch, an economist at S&P Global Market Intelligence and author of the Bellwether report, explains that the rebound in marketing budgets occurred as marketing executives “concentrat[ed] efforts on revenue-generating sectors and prioritis[ed] targeted, client-driven campaigns — including more events — to better position their organisations amid ongoing headwinds and uncertainty.”

Chamber further advises: “Moving into 2026, advertisers and brands must avoid overcorrecting towards performance-led thinking. Instead, with adspend forecasts improving but wider economic growth subdued, brands should focus on resilience.

“That entails maintaining a balanced media mix, investing in measurement that captures both short- and long-term impact, and using channels like Events and PR to compliment, but not substitute, sustained brand investment.”