Video investment drives modest growth in main media spend, says Bellwether

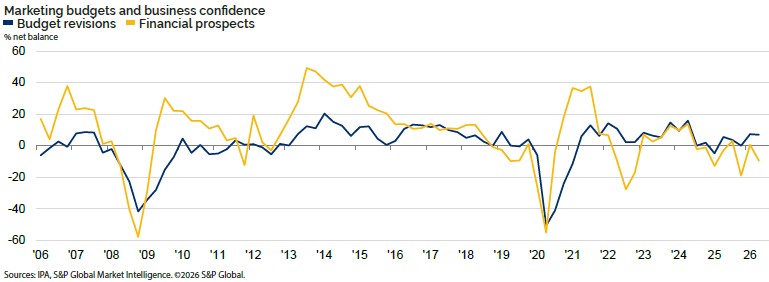

Total marketing budgets remained resilient in Q2 despite a decline in business and market confidence amid continued war in the Middle East and its knock-on effects on global inflation.

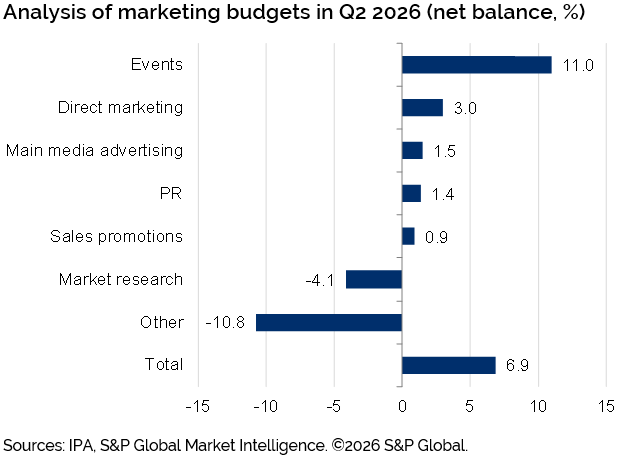

That is according to the latest IPA Bellwether report, which found that a net balance of +6.9% of brands increased their marketing spend in Q2.

The biggest beneficiary of budget increases was once again events (+11% net balance), as it was in Q1. This is followed by more modest growth in direct marketing (+3.0% net balance), main media advertising (+1.5% net balance), PR (+1.4% net balance), and sales promotions +0.9%) budgets.

In contrast, a net balance of Bellwether respondents reported trimming market research (-4.1% net balance) and “other” activities (-10.8% net balance).

The increase in marketing budgets occurred even as panellists reported increasing fears of macroeconomic instability impacting both their individual businesses and their industry’s financial prospects.

The survey was collected between 1-23 June, before both UK Prime Minister Keir Starmer’s announced his resignation and before a memorandum of understanding to cease hostilities between the US and Iran was agreed and subsequently breached. This week, the US renewed military strikes on Iran and President Trump said the US would reinstate its maritime blockade of the Strait of Hormuz, charging ships a toll in return for claiming to provide safe passage.

Bellwether survey respondents widely agreed the war in the Middle East has created a global inflation shock, disrupted supply chains and created a drag on investment activity.

“Everything is still uncertain,” said one FMCG marketer. “We are forecasting in a volatile market and that makes everything unpredictable.”

The net balance of Bellwether panellists predicting better financial prospects correspondingly fell to -9.6% in Q2, compared to +0.6% in Q1, with nearly one-third (32.3%) of respondents saying they felt less upbeat about their financial outlook than they did three months ago. Meanwhile, a net balance of -25.1% of respondents said they anticipated better financial prospects for their industry as a whole.

A much-awaited return to brand building?

Maryam Baluch, the Bellwether report’s author and an economist at S&P Global Market Intelligence, commented that “the fact there hasn’t been a considerable scaling back of activity in response to the economic shock arising from the Middle East war suggests firms are taking a strategic, longer-term view rather than getting bogged down in short-termism.”

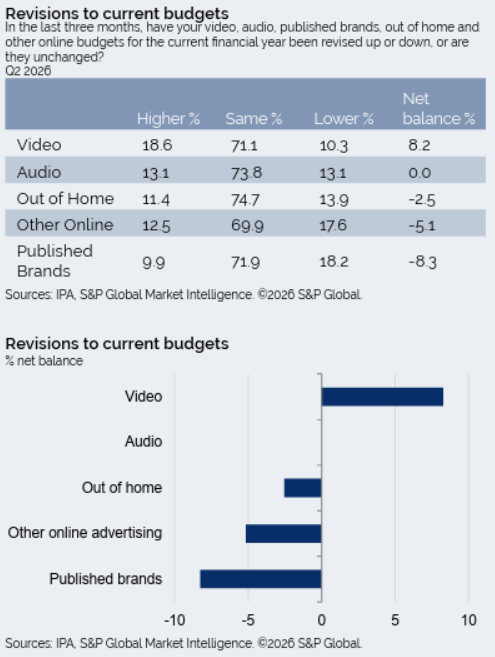

This is demonstrated, she argued, by the shape of budget changes in the Bellwether‘s main media segment. Main media budgets’ upward revisions were driven entirely by a net balance of +8.2% of businesses growing investment in video, the highest upward budget revision to the category since Q4 2024.

This is compared with flat growth in audio budgets (0.0% net balance) and declines in OOH (-2.5% net balance), other online (-5.1% net balance) and published brands (-8.3%).

It is the first time the other online category has seen a contraction in marketing budgets since Q3 2024, and relative to the +5.7% upward revision in Q1, it is the most pronounced contraction in other online budgets in nearly six years.

OOH, meanwhile, has now seen eight consecutive quarters of contractions. Audio, which had fallen in the past 12 quarters, stabilised in Q2.

“The overriding message from this quarter’s report is that UK companies continue to recognise the value of advertising,” IPA director general Paul Bainsfair commented. He said he was particularly encouraged to see strong growth in video advertising budgets alongside cuts to short-termist other online activity, which he took as evidence that “businesses understand the importance of investing in long-term brand building”.

Despite the optimistic budget revisions, Bainsfair added it is “understandable” that businesses’ financial confidence has waned in Q2. “Amid geopolitical turmoil, ongoing heightened inflation, supply-chain disruption, not to mention political upheaval closer tohome, it makes for an undeniably tough and uncertain environment in which to operate.”

He continued: “In light of such challenges, it is therefore more important than ever that companies play the long game and continue to invest in brand-building media that is proven to be better placed to drive sustainable business growth.”

Balancing the long and short of it

It is plausible Q3 continues to offer a more optimistic picture for UK media investment. As Publicis Media COO Mark Howley commented, England’s strong FIFA World Cup performance could provide a “better-than-anticipated Q3 trading environment”, leading to higher growth than originally forecast.

Continuing with the football metaphor, Jim Kelly, deputy MD and head of planning at creative agency Story called the latest Bellwether report a “game of two halves”. He offered: “On one hand, it’s highly encouraging at a headline level to see just how resilient the sector appears to be despite the never-ending turbulence both domestically and internationally.”

On the other hand, Kelly is less convinced than Bainsfair that the Bellwether provides evidence of increased brand investment. “With the healthiest increases being reported in events and direct marketing, this indicates a perhaps understandable focus on lower funnel conversion,” Kelly argued. “Meanwhile, many main media budgets are reported as contracting, and my underlying worry remains that long term brand investment is taking a back seat to the short-term commercial outcomes.”

As the debate over short-termist pressures and long-term goals persists, Kelly concluded: “The final result? It’s probably a draw right now.”