Publishers advised to be ‘niche at scale’ amid the winding road to Google Zero

Publishers “don’t need to be everywhere”, but rather must prioritise direct audience relationships and hone a distinctive voice to thrive in the AI-era.

That is according to a report published by the Professional Publishers Association (PPA) and Enders Analysis and presented at the PPA’s annual Festival this morning in London.

The report, Humans and Machines: The Everywhere Equation, analyses how AI is remaking the publishing business model, and makes several arguments for how publishers should proceed.

These include looking to develop “niche at scale” content strategies, such as through adopting a “hub-and-spoke” model offering both depth and breadth.

It notes that AI is making trusted editorial brands more important in a world of “infinite content”, but that discoverability and distribution has become harder as generative AI erodes clickthrough rates from search and news consumption habits continue to favour social media platforms.

“While technology continues to reshape how audiences discover and consume content, some fundamentals remain constant,” commented PPA CEO Sajeeda Merali. “People seek belonging, trusted voices, and meaningful connection. These are qualities AI cannot replicate, and where trusted editorial brands have a clear and enduring advantage.”

‘Engagement, habit, community’: Publishers advised to seek ‘defensible’ strategies in new search era

Search erodes, alternatives in flux

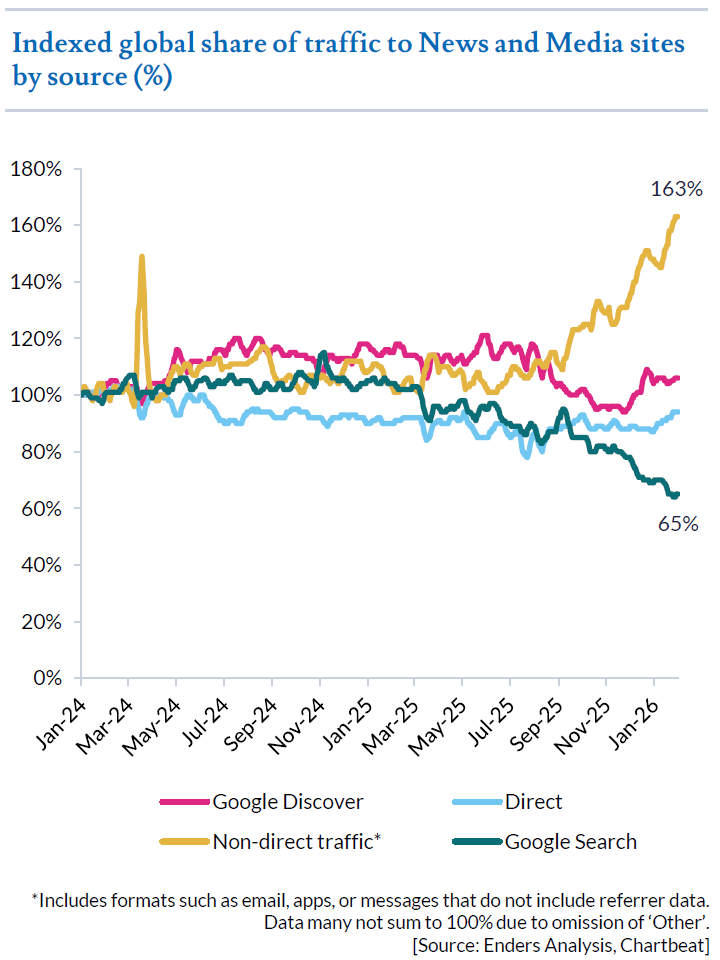

Search is now “no longer a reliable growth engine for publishers”, the report plainly finds, with Google Search referalls falling by one-third globally between November 2024 and November 2025.

This has particularly affected smaller publishers, which collectively have faced -60% declines in search referral traffic in the past two years compared to -22% for larger publishers.

Publishers have broadly responded by deprioritising efforts in search as well as some social platforms, like X, that have eroded support for news. Instead, they have prioritised building direct relationships with audiences on YouTube, AI platforms, and owned channels such as newsletters.

Events and memberships have also both grown in importance for publisher business models, while apps and product experience now “matter more than ever”.

“The road to ‘Google Zero’ is winding […] but the revenue impact of AI-mediated search will only compound,” the report warns.

A decline in referral traffic from search has led to a further erosion of digital advertising models, which had already “fallen out of bed” following similar rug pulls from social media giants, overzealous keyword blocklisting practices from advertisers, and a relatively meagre take compared to print revenues.

Rather, Enders advises that subscriptions remain “the most robust monetisation strategy” for publishers of all sizes, as they retain more control over such a business model than advertising strategies that “have struggled to translate declining print value online.”

The move to embrace direct audience relationships rather than chasing referral traffic has knock-on effects for content strategy. As Alan Loader, chief media officer at The Channel Company, commented during a panel discussing the report at the PPA Festival, “Content which we know to be a bit generic, a bit filler, we need to stop.”

That said, the report warns that consumers are facing subscription fatigue and constraints on willingness to pay, particularly amid a vast increase in supply of independent efforts made possible through newsletter platforms like Substack, Beehiiv and Ghost.

As such, advertising will remain “critical to many consumer-facing publishers” either as a primary or supplementary business model, with digital ad revenues remaining relatively stable even as print ad revenues broadly decline.

The report notes that while the UK ad market appears as though it has never been stronger, total ad market growth figures hide that “a notable share of that strength” is funnelled toward US-based tech platforms. This development has “maroon[ed] the publisher opportunity”.

Indeed, while AA/Warc’s 2025 adspend report found the UK ad market grew 6.4% in 2025, published media saw declines at both national (-4.6%) and regional (-6.0%) news brands, as well as magazine brands (-5.1%).

Hub-and-spoke, depth and breadth

The irony is publishers remain increasingly reliant on platforms for discovery. As the report concludes, “a multi-format presence is critical for reach”.

Publishers are advised to be “niche at scale”, building moats through first-party data strategies and a “defined audience voice, purpose and depth through owned formats and IP” before extending that content broadly. Enders likens this to a “hub-and-spoke” model, servicing existing consumers with depth while developing breadth across platforms as a pipeline for future audiences.

“Discoverability is shifting from being found to being chosen […] Platforms now both consume and distribute: publishers must optimise for each platform’s structure, and a multi-platform approach cannot be an afterthought,” the report reads.

There are risks inherent to efforts at improving breadth via social publishing, with publishers widely considering three models: building in-house studios, acquiring existing studios, or partnering with creators via a revenue-share system.

Enders warns that while publishers are seeking to increase “personality-driven” journalism to foster a sense of community and create appeal on social video platforms, an “overreliance on a single personality” creates risk. The Washington Post, for example, lost 85% of its YouTube views in the four months after the departure of popular creator Dave Jorgenson, who now runs his own infotainment outlet, Local News International.

Publishers welcome government walk back on opt-out copyright exception for AI companies

Enders Analysis CEO Claire Enders summarised the state of play as: “the ground is shifting […] but a response is taking shape”, with the most successful publishers “investing in direct relationships, distinctive voice, and the formats and communities that machines cannot replicate.”

“What is plain is that these publishers are doing what the best publishers have always done: knowing their audiences precisely, investing in human expertise, and refusing to compete on terms the economics do not support,” she continued.

“Trust, in a contested information environment, is not a soft asset. It is the asset.”