UK adspend increased 6.4% in 2025 as AA/Warc updates data presentation

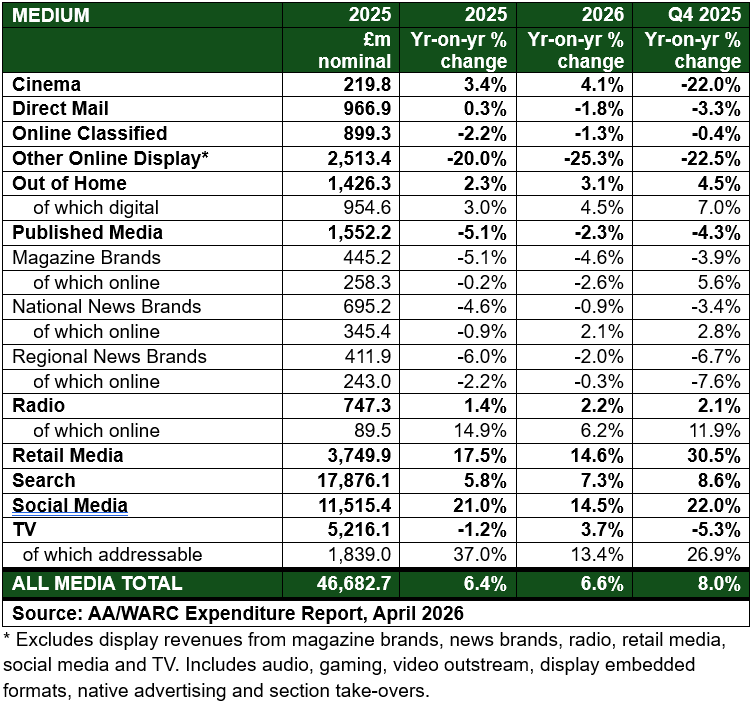

Advertising expenditure rose 6.4% year on year in 2025 to reach £46.7bn, the latest AA/Warc Expenditure Report has found. In real terms (after inflation), advertising expenditure grew by 2.9% year on year.

The report offers a refreshed look at the health of the advertising industry. Following consultation with a forum of industry leaders, including representatives from trade bodies such as the IAB, Thinkbox, Radiocentre, Newsworks, the PPA and the IPA, AA/Warc has made three changes to its reporting practice.

The Expenditure Report now offers public deduplicated media totals, standalone categories for social media and retail media, and a new definition for “TV” that James McDonald, Warc’s director of data, intelligence and forecasting, says better reflects changes to TV trading practice.

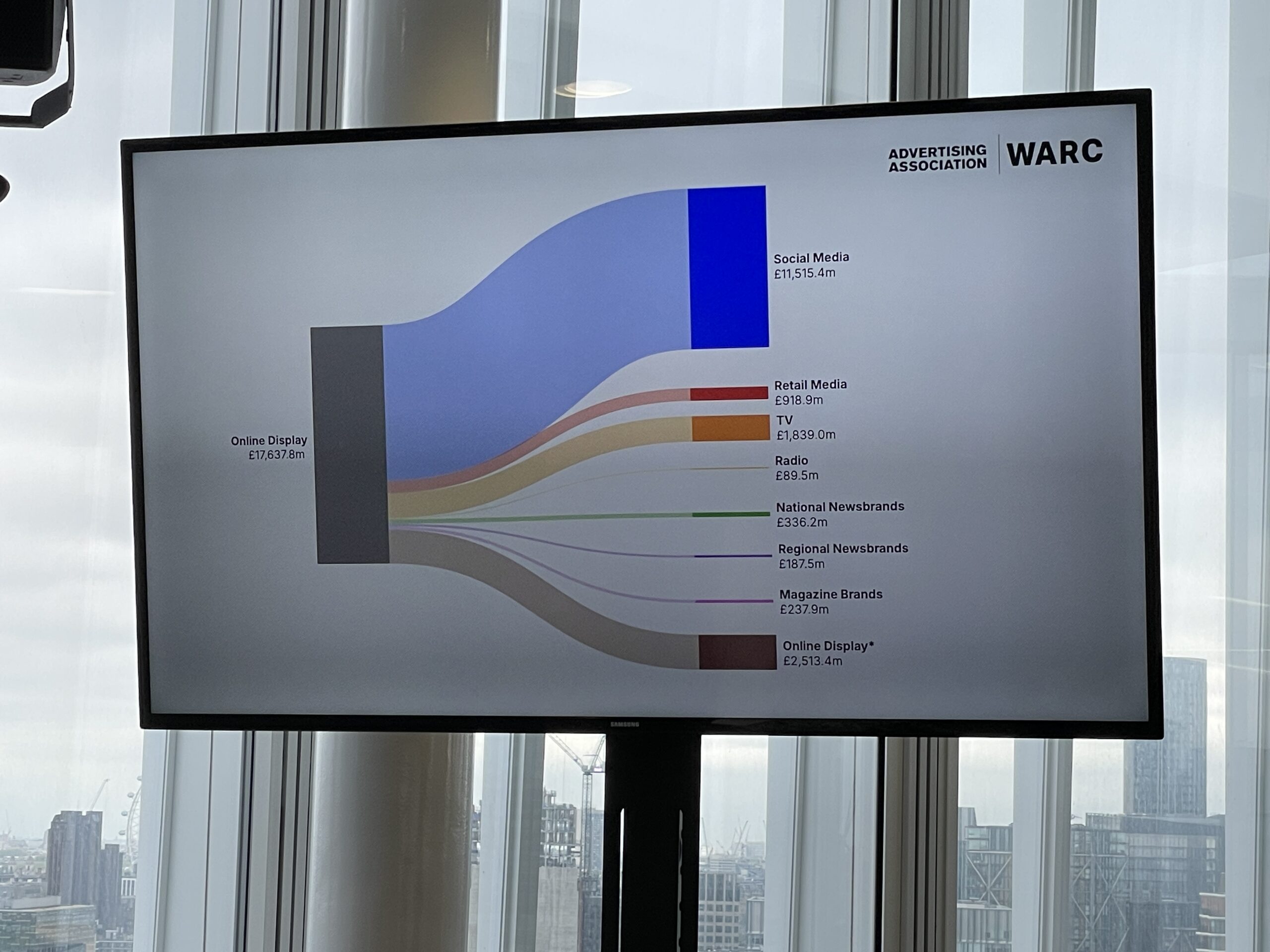

Under the new reporting, online display is now broken out into its constituent parts, offering more granular public data about different aspects of the online advertising ecosystem.

The changes were universally praised by trade body leadership at a preview event held by the Advertising Association and Warc at News UK in London on Tuesday.

TV is now measured both as a total TV figure and an addressable TV figure. AA/Warc notably categorises YouTube as social media rather than TV for measurement purposes.

Addressable TV is defined as “a buying mode that allows marketers to target specific audiences, households, or individuals with precision within the high-quality, trusted environment of TV,” a description borrowed from Thinkbox.

The new reporting presentation “allows nuances in our industry to be communicated with greater clarity,” McDonald explained at the preview event.

Advertising Association CEO Stephen Woodford added that the AA/Warc Forum will continue to meet as part of an ongoing consultation effort with industry stakeholders to consider further changes to reporting practice.

As Woodford previewed, the group is already considering how to better present influencer adspend as distinct from paid social campaigns, adspend attributable to AI search within large language models (LLMs), and splits between different-sized advertisers.

The latter is significant, as the long tail of small- and medium-sized enterprises (SMEs) has driven much of the adspend growth, which has been largely captured by global online platforms, though other media owners are increasingly pursuing these businesses.

Radiocentre head of insight Donna Burns added that the audio industry trade body is keen to collaborate with the IAB to create a “total audio” figure to report, which would presumably include AM/FM and digital radio, as well as streamed music and podcasts.

Channel breakdowns

AA/Warc’s new reporting presentation shows that, for full-year 2025, double-digit growth was recorded across addressable TV (+37.0% to £1.8bn), social media (+21% to £11.5bn), retail media (+17.5% to £3.7bn), and online radio (+14.9% to £89.5m).

Search also grew 5.8% to £17.9bn, remaining the largest media channel and accounting for nearly two-fifths (38%) of the UK ad market. Its market share is followed by social media (24.7%) and TV (11.2%).

Other channels that grew in the single-digits last year included cinema (+3.4% to £219.8m) and OOH (+2.3% to £1.4bn).

In contrast, published media (-5.1% to £1.6bn) continued to suffer year-on-year declines, including across national (-4.6%) and regional (-6.0%) news brands, magazine brands (-5.1%), and their online editions. Total TV adspend also declined 1.2% to £5.2bn.

Overall growth notably picked up as 2025 progressed, with Q4 a particular bright spot. Adspend totalled £12.9bn that quarter, an increase of 8.0% year on year, with growth again driven by retail media (+30.5%), addressable TV (+26.9%), and social media (+22.0%).

AA/Warc forecasts further growth of 6.6% in 2026, to reach £49.8bn. However, McDonald warned of the “elephant in the White House”, referencing US President Donald Trump and the US-Israel war with Iran, which has created macroeconomic headwinds, including increased inflation as a result of higher energy prices.

However, McDonald said “the year has started well”, noting there is no evidence yet that the war has resulted in an economic shock. Citing the latest IPA Bellwether report, he noted that business confidence has remained buoyant, leading to rising marketing budgets.

Should AA/Warc’s latest 2026 adspend forecast come to fruition, the UK’s advertising market would have doubled in size in just six years.

As IPA director of media affairs Nigel Gwilliam commented at the preview event, this has occurred even amid sluggish UK GDP growth, which has largely hovered between 0% and 1.5% following the post-pandemic recovery.

Since the Covid-19 pandemic, advertising investment, which historically tracked UK GDP, has significantly outpaced GDP growth, raising concerns about the health of the UK’s media industry.

Gwilliam argued that this development is another “elephant in the room”: a large and growing share of the ad market is now captured by US-based tech companies rather than UK-based media owners, with downstream implications for the wider British economy.

‘Bullish start to the year’: Media budgets rose in Q1 despite chaotic geopolitics