How do TV networks capitalise on the digital stumble?

Opinion

The Attention Council CEO Andy Brown and media analyst Ian Whittaker have joined forces to launch a White Paper arguing for three key requirements for advertisers to evaluate TV alongside digital video.

Over the past six months, there has been a noticeable step-up in the level of investment into the media measurement industry, particularly from the private equity space. The $16bn purchase of Nielsen, together with the $325m investment by Goldman Sachs into TV measurement business iSpot, has highlighted the growing interest in the space.

However, the rationale for these investments has somewhat changed. Previously, the PE interest in these names seemed to stem from an interest in monetising the scale of ‘data’ these firms held. The successful transformation of firms such as YouGov from a low-growth market research business to a higher-growth data and analytics style business heightened interest in these names as similarly suitable for a refocus.

Investments are being driven by an interest in measurement specifically. That should not come as a surprise, given several trends have come together at once.

The first is the move away from cookies together with Apple’s privacy changes which are leading to disruption in the online advertising markets. While Google delayed the elimination of third-party cookies to 2024, it will eventually come; the increasing torrent of privacy-focused legislation and regulation from Europe and California has accelerated change. Meanwhile, Apple’s changes on privacy are having a meaningful impact on the social media businesses in particular, with the slowing growth of Meta, YouTube and Snap, to varying degrees, bringing home to investors that these changes are having a meaningful business impact.

The second is that the traditional boundaries of “analogue” and “digital” media are breaking down as a greater proportion of platforms’ revenues come from digital. The majority of publishing revenues, as well as outdoor, now come from digital, at least in most established markets. The most pressing change has been the embracing of advertising video-on-demand (AVOD) services by the major broadcasters and networks globally, particularly in North America and Europe. This is making a meaningful change to broadcasters’ growth rates — especially in Europe.

The traditional metrics of TV measurement do not necessarily work well in the AVOD world and, as the percentage of revenues from AVOD grows, so does the demand for more accurate measurement systems, especially given that AVOD brings a different audience to the Broadcasters. The move by the US networks to bundle in linear TV and AVOD together at the upfronts despite the opposition of media buying groups, whose internal television buying teams are still set up to deal with the traditional TV model — has highlighted the need for improved measurement solutions that can accurately handle such “hybrid” media.

The third issue, and related to this, is the move by the streaming services such as Netflix and Disney+ — the largest global services — to embrace advertising as subscriber growth momentum slows, which has raised questions about their future profitability and, perhaps more importantly, their valuations. Netflix’s share price has dropped over 60% over the past 12 months and its disastrous Q1 results, which saw not only subscribers fall in Q1 but also the company give guidance of a two million subscriber loss in Q2, has persuaded management that both new revenue streams and a new message for the markets need to be introduced. While the relatively small audience share numbers of Netflix (it has just over 6% of total TV viewing time in the US) means that the revenue uplift may be limited in the overall context of Netflix’s total revenues, the very high drop through rate means it could make a meaningful difference on the profits front. Given this move is likely to happen quickly (more so in the case of Disney+ than Netflix in all probability), it has increased the importance of introducing measurement systems that can accurately reflect their audiences.

Lack of ad measurement standard holds back spend

Lying behind all of this is the desire from advertisers to have a unified measurement platform that makes it simpler to compare the cost and effectiveness of different media platforms instead of the current “apple and pears” system.

This is also not just a theoretical issue. The lack of an accurate, and accepted, unified measurement system is one of the key reasons why boards and CFOs/CEOs, while theoretically understanding the importance of brand advertising, do not trust the effectiveness of advertising spending (especially brand advertising) and so can be hesitant to sign off on extra advertising spend.

One of the core reasons why the tech giants have made such strides in capturing such a large chunk of ad spending is their promise that they can demonstrate the outcomes of spending on their platforms almost in the way of a scientific formula. We should sceptical of such claims — as any financial analyst will tell you, the core to any model is not the output, but the inputs and how they have been formulated.

It also has significant implications for advertisers in terms of wasted adspend and, ultimately, lost shareholder value, which is the ultimate concern of boards and management teams. Using the GroupM estimates going out to 2026, the lost shareholder value from wasted adspend is around $2.25tn, a colossal amount of lost value. This is a culmination of (primarily) an imbalance between Search and Brand advertising revenues, the so-called “ad tech” tax, potential fraud and other wastage in the system.

There is a clear case to argue that a vastly improved measurement system would lead to a reduction in this lost value.

There is a game-changing rationale for the broadcasters (and outdoor, which is also increasingly video-based) to move to a common measurement system. The way that the debate over such unified systems has often been framed is that of a one-way street where such a standard can only lead to the broadcasters losing an ever-increasing share of advertising money to the tech companies. Not only does this reflect a latent pessimism amongst the broadcasters about the effectiveness of their own products, but also misses the reality: this has the opportunity to be a two-way street where such a standard actually gives an opportunity for broadcasters to take a share of the growing online video advertising market.

The potential uplift for the broadcasters could be enormous. Again, based on the GroupM estimates, if 10% of online spending (not including Search) moves across to broadcasters, then that would boost up global amount of broadcasters’ advertising revenues by over $50bn per annum over the medium-term on GroupM forecasts (for outdoor, while the absolute amounts of any shift would be less dramatic, the relative improvement would be far greater given its smaller size). That figure is also likely to be conservative because it does not take into account a potential shift of revenues out of Search from a more accurate and common measurement system.

That may seem optimistic but there are a number of reasons for suggesting it is credible. Broadcasters should be seen not as traditional TV providers or outdoor companies, but more as video content distributers that are platform-agnostic. There is no reason why broadcasters should not be in a position to capture significant amounts of online video advertising dollars.

In some ways, ‘traditional’ media owners have several major advantages. The Apple privacy changes have brought about a significant level of doubt over the level of effectiveness of platform services such as Facebook and YouTube that was not there before. Linked in with this, the changes — together with the phasing out of cookies — has forced advertisers to exit the comfort zone of continuing as normal and instead has given the smart ones an opportunity to reassess how they spend advertising money. Finally, both the broadcasters and outdoor companies bring a level of brand safety/reputation that is not matched by the tech platforms.

Therefore, both the current investor interest in measurement is rational and the current situation represents a major opportunity for the broadcasters (and potentially other “traditional’ media) to capture a share of the online video advertising budgets if they can find the right measurement strategy.

Let’s look in a little more detail as to how the measurement ecosystem is evolving (as we move into a multi-currency world). There are numerous major trends that are impacting the measurement ecosystem e.g. we do not address here the impact streaming is having on panel solutions for TV or indeed the rapid and heavy investment in the TV networks first party data ecosystems from ad serving technology, through to identity systems and data clean room technology.

Here we have pulled out three areas that that are arguably key requirements for advertisers to evaluate TV alongside digital video. We have summarised the approach as the 3 A’s.

Audience measurement

How can an advertiser be sure that the audience that is offered by TV is efficient and driving unique reach (versus digital video)? Indeed, how do they avoid excess frequency?

As mentioned above, the inability to look at digital video such as YouTube on a common measurement platform with TV (whether that be linear or streaming) makes budget allocation unnecessarily difficult, let alone being able to adjust a campaign in flight across the two major media channels. This has become a critical plank of the WFA agenda. It has resulted in the advertiser directly-funded research cross screen measurement initiatives in UK, US, Canada and most recently Germany.

In the US, the somewhat challenged Nielsen has set off down a path to provide cross screen metrics via the Nielsen One initiative. The UK initiative from the advertiser body ISBA, Project Origin has been met with numerous challenges from both a management and a financial perspective, with rapid changes in CEO (although there is significant hope with the hiring of ex-agency CEO Tom George). In addition, there has reportedly been limited or even zero financial support from the UK TV networks for Origin, which has significant support from the digital behemoths Google and Meta.

Yes, there has been investment in audience research from the TV networks in recent months. But it has tended to focus around the measurement of streaming (BVOD) and their own first-party data initiatives, such as the excellent pan-broadcaster initiative C-Flight. But, whilst C-Flight has provided valuable insights across the linear and streaming delivery on campaign performance across TV, it still falls short on meeting the advertisers goal of seeing the total audience delivery of their campaign across TV and digital video in combination. BARB now reports on the consumption of YouTube on UK industry currency it is not at a campaign or even content-level which is what advertisers are seeking.

The objections put up by the broadcasters to failure to support Project Origin and its ilk, are many and range from brand safety through to the fact that the viewing experience of TV is innately different (and, they would argue, superior to that of digital video). The fear of the broadcasters around cross screen measurement is perhaps less about the impact of combined reach and frequency, but more about commoditisation of impressions data.

A new research approach might provide some hope for the future. One such research approach is the advent of attention-based metrics.

Attention measurement

Attention metrics are arguably the fastest growing area of interest for the media industry (one of the authors must declare an interest as CEO of industry lobby group The Attention Council). The principle behind attention metrics are quite simple: humans have a finite amount of attention that they can give to a person, a media channel, or even an ad.

The last decade has seen a massive explosion in media content and the associated number of ad exposures. It is intuitive that advertising has to work harder to stand out in the clutter. This broad concept is known as the attention economy.

So how do we measure attention in this new world? The range of methods are quite varied, ranging from neuroscience through facial recognition to the use of gaze technology. Much of the early UK work was pioneered by leaders in the space such as Prof Karen Nelson-Field, Yan Liu, Mike Follett, and others.

Perhaps the earliest adopter of attention metrics on the buy-side of the industry was Dentsu, which, via their “Attention Economy” study, created relative attention scores across media types. The agency group then integrated this with several audience sources to provide a planning tool that work across media. The result is that all impressions are not created equal and although anecdotally it is not always cheaper buying on an attention basis, it has been seen to deliver, in terms of the effectiveness driving at all levels in terms of “the funnel.”

Whilst more experimental design work (as opposed to case studies) is required on the appropriateness and limitations of the methods used, attention measurement can be applied as a way not only to move measurement from opportunities to see ads to what has actually been seen, but also to value in relative terms of the TV impression versus those of digital video. When factoring attention and cost, there is evidence that TV will stand up well when put side by side on an attention basis.

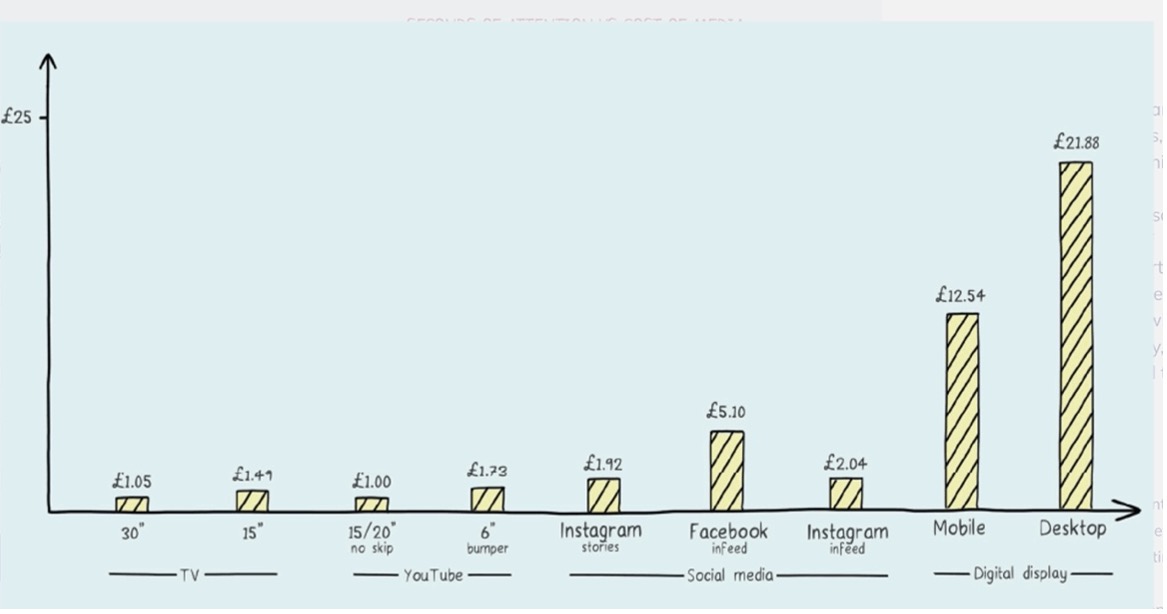

Table 1 – Cost per attentive second by media format. Source: Ebiquity/Lumen/TVision “The Challenge of Attention”

It has recently been announced by TVision and Lumen that they will be launching a cross media attention measurement solution including a monitored TV attention panel. The authors are encouraged by the recent engagement with attention measurement by Thinkbox.

Attribution measurement

One of the biggest changes in TV measurement (at scale in the US) is attribution. That is to say, moving beyond how many people were exposed to the ad, to look at the impact of the ad.

Specialist companies such as TV Squared (now part of Innovid) are able to look at impact of each spot that airs and link that to an outcome often behavioural and based on Web metrics ranging from search to web traffic.

Attribution is relatively new to TV but is widely used in digital media evaluation. In the US many TV sales staff at the major networks have been trained in attribution techniques and sell packages of TV inventory linked to an outcome (or attribution) report. Arguably this has contributed to direct to consumer (DTC) one of the fastest growing ad categories in the US and now in the UK. A number of UK networks are beginning to offer attribution resources for advertisers Sky work with the aforementioned TVSquared, whilst Channel 4 have recently announced an attribution partnership with Viewers Logic.

For more advanced clients and to show the comparability of the TV effectiveness versus digital, the approach used might be multi-touch attribution (MTA) to determine the contribution of each media channel to a sales or brand outcome. The challenge of this approach is that the deprecation of cookies, makes the tracking of the path to purchase more challenging and ultimately higher-level modelling such as market mix modelling (MMM) might be deployed.

The question with both MTA and MMM is whether the TV network would take on the additional costs to demonstrate the contribution of TV to the overall campaign, without knowing the outcome of the study. That said, Thinkbox has done excellent work in the area to create norms for TV performance versus digital.

Summary

It is clear that the world of TV measurement is undergoing perhaps more change than at any point since the introduction of the peoplemeter over 40 years ago. There is greater investment in new tools and techniques that may provide an excellent opportunity not only for investors in these new solutions, but also for a mature medium like TV to counter the ongoing swing of ad expenditure to digital media.

Andy Brown is CEO of The Attention Council, a non-profit organisation that aims to advance “the next generation” of measurement, and former CEO of Kantar Media.

Ian Whittaker is a media analyst and founder of advisory firm Liberty Sky Advisors.

They will discuss this White Paper in more depth at The Future of Media tomorrow.